Backtesting built by traders

& API development

Deep dives, tutorials, and market research from the team building the stocks and options data API for developers and systematic traders.

More Articles

Build an Options Chain Scanner That Is Quote-Aware

Build quote-aware options chain scanners with expirations, DTE, moneyness, Greeks, IV, OI, spread percent, quote age, pagination, quotes, and trades.

Historical Options Replay for Event Studies

Replay events with point-in-time contracts, quote windows, trades, IV crush, spread filters, rejects, and audit artifacts.

Real-Time Options Data Architecture

Design live options systems with REST snapshots, WebSockets, quote freshness, entitlements, reconnects, REST backfills, and alert evidence.

Stock and Options Data Joins for Strategy Research

Join stock bars, trades, quotes, snapshots, and indicators with option expirations, chains, contracts, OCC symbols, and paper artifacts.

REST vs WebSocket Market Data API Guide

Compare REST snapshots, historical windows, WebSocket streams, backfills, local caches, freshness labels, and entitlement gates for market-data systems.

Historical Market Data Ingestion and Cache Design

Design historical market-data caches with source requests, cache keys, pagination, entitlement labels, quote windows, replay artifacts, and reject reasons.

Market Data API Due Diligence Checklist

Evaluate market-data APIs by workflow, access method, source clarity, timestamps, pagination, entitlements, commercial use, support, and artifacts.

Market Data Timestamps and Trading Sessions API Guide

Handle UTC, ET, session labels, quote age, completed bars, WebSocket event time, backfills, and timestamp artifacts in market-data systems.

Missing Market Data and Corrections Provider Checklist

Evaluate missing rows, corrections, condition codes, late prints, empty windows, no-bid options, pagination gaps, and data-quality rejects.

Option Quote and Trade Condition Codes: API Guide

Use option quote conditions, trade condition codes, exchange ids, corrections, sequence numbers, timestamps, and reject policies in scanners and backtests.

Unusual Options Activity Scanner Developer Guide

Build unusual options activity scanners with volume, premium, open interest, DTE, moneyness, quote quality, trade review, score artifacts, and reject reasons.

Options Volume and Open Interest in Unusual Activity Scanners

Understand options volume, open interest, volume/OI ratio, premium, DTE, moneyness, quote quality, and scanner interpretation limits.

Options Flow False Positives in Scanner Alerts

Avoid overreading options flow with spread checks, quote age, trade review, event context, multi-leg caveats, reject labels, and scanner artifacts.

Stock Trades vs Stock Quotes API for Developers

Separate stock trade prints, last trade, bid/ask quotes, quote age, aggregates, snapshots, and plan entitlements before building dashboards or backtests.

Historical Stock Aggregates and Indicators API Guide

Use adjusted bars, open-close records, grouped bars, SMA, EMA, MACD, RSI, bar timestamps, and option handoffs without confusing signals and fills.

Real-Time Stock Data Watchlist Architecture

Design watchlists with ticker reference, snapshots, movers, trades, quotes, bars, freshness labels, stale rows, REST backfills, and entitlement logging.

SPCE, SpaceX, and the Meme-Stock Backtest Problem

A market-data research note on the SPCE run-up: Virgin Galactic catalysts, SpaceX IPO confusion, Reddit attention, GameStop comparisons, and how to backtest it without fooling yourself.

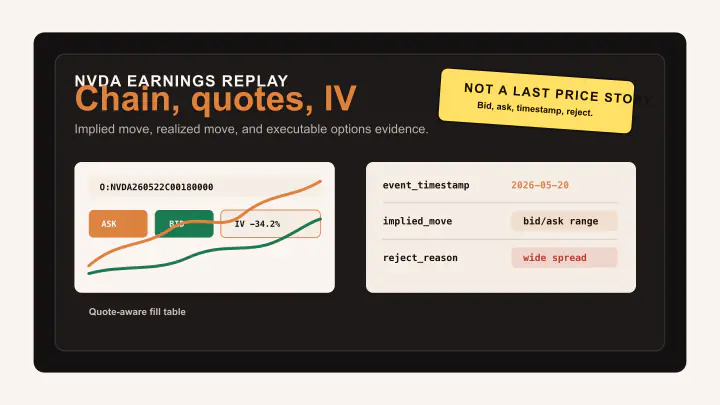

NVDA Earnings Options Replay: What the Chain, Quotes, and IV Actually Said

A quote-aware NVIDIA earnings replay: implied move, realized move, IV crush, exact contracts, tradability, and why last price is not enough.

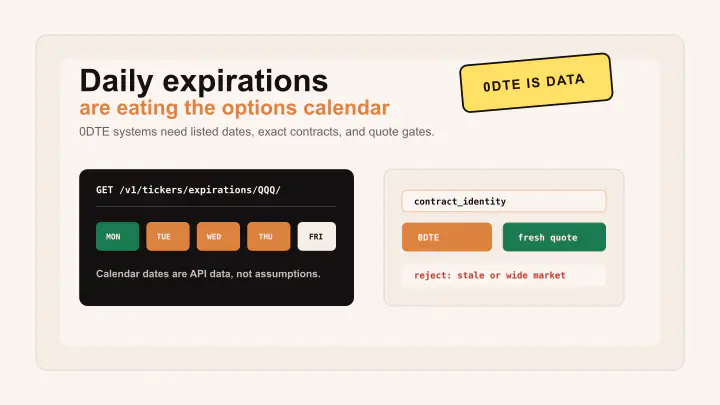

Daily Expirations Are Eating the Options Calendar

Cboe DJX daily expirations are a market-structure hook for the real developer problem: short-dated options need expiration discovery, exact contracts, quotes, and calendars.

Paper Trading Is Live in CuteMarkets

CuteMarkets now includes integrated paper trading with paper accounts, stock and option orders, positions, fills, portfolio history, and quote-aware simulated execution.

R124/R130 Bull Seagull: A New Paper-Promotable Model Family

The May 15 R124/R130 QQQ bull seagull cleared P0 paper-promotable gates, with common paper-trading issues now going into an integrated paper module.

Model-Family Search: The Tuesday No-Go Report

The May 12 model-family search rejected UOA variants, public-source branches, put-flow ideas, fade mechanics, and near-miss combinations.

The Developer's First Backtesting Loop: Start With Evidence, Not Optimism

A developer-first introduction to causal options backtesting: signal timestamps, point-in-time contracts, quote-aware fills, and artifacts.

What To Log Before Optimizing a Backtest

Before tuning parameters, log signal timestamps, selected contracts, quote evidence, rejects, manifests, and summary metrics.

Same-Bar Fills: The Lookahead Bug Developers Keep Rebuilding

Completed bars can create signals, but they should not also grant intrabar fills unless standing order state is explicitly modeled.

Point-in-Time Option Contract Selection

Options backtests need contract selection from the historical universe visible at the decision timestamp, not from a modern chain.

Quote-Aware Options Backtests Need Bid, Ask, and Rejects

Realistic options replay should use bid/ask quotes, quote age checks, spread limits, and explicit reasons for rejected trades.

Opening Range Breakout Backtesting for Developers

ORB research exposes the core developer problems in trading backtests: range definition, causal entry, DTE, stops, and fills.

VWAP Mean Reversion: Signal Quality vs Trade Density

VWAP mean reversion research must balance selective signal quality against enough trades and active days to trust the result.

Dispersion and Relative Strength Backtests Need Proxy Discipline

Proxy-based strategies need strict bar alignment, causal beta context, and option execution checks before relative strength claims matter.

Choosing DTE Buckets in Options Research

DTE buckets connect signal horizon to listed expirations, liquidity, gamma exposure, spread behavior, and paper readiness.

Walk-Forward, PBO, and DSR for Trading Developers

Use walk-forward validation, PBO, and deflated Sharpe to test whether strategy selection is stable or just lucky.

How To Read a No-Go Backtest

A no-go report is a research asset when it separates launch integrity, data coverage, execution, concentration, and robustness.

Building a Portfolio of Trading Sleeves

A trading sleeve should improve the combined book, improve more than a standalone backtest chart.

Backtest to Paper Trading: The Parity Checklist

Freeze the research object, replay benchmark sessions, compare decisions, and preserve reject reasons before paper trading.

Paper Bot Data Feeds: Live Bars, REST Backfills, and Fail-Closed Logic

Paper bots need explicit policies for provisional live bars, completed-bar backfills, signal age, and option route rejects.

Unusual Options Activity Backtesting Needs Exact Contracts

UOA research needs exact contract triggers, quote-strict fills, threshold families, and clear prior-OI caveats.

Liquidity Filters in Options Backtests

Liquidity filters define whether a strategy could plausibly trade: quote freshness, spreads, volume, OI, DTE, and price guards.

Position Sizing, Drawdown Caps, and Strategy Promotion

A candidate should be promoted with weight frontiers, drawdown caps, robustness checks, and an operational sizing decision.

Backtest Artifacts, Manifests, and Launch Contracts

Manifests, selected trades, daily PnL, diagnostics, and launch contracts make research repeatable and paper-ready.

API Data Objects Backtesting Developers Actually Need

Backtesting developers need contracts, expirations, quotes, trades, aggregates, snapshots, and reference data in the right order.

A Developer Roadmap for the First 30 Days of Backtesting

Spend the first month building causal replay, quote-aware fills, reject logs, artifacts, robustness checks, and paper readiness.

UOA Exact-Contract Backtests: Strong PnL Was Not Enough

The May 8 UOA exact-contract pass showed strong local quote-priced PnL, then failed robustness and remote holdout checks.

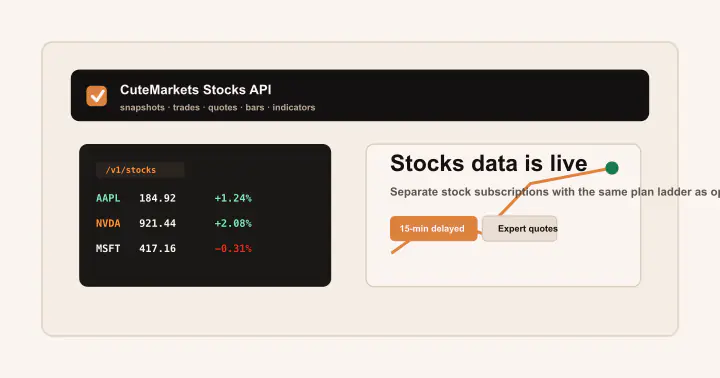

Stocks Data API Is Live in CuteMarkets

CuteMarkets now supports stock REST endpoints with separate stock subscriptions, Developer delayed access, Expert live access and quotes, and one account for options and stocks.

How to Build a Paper Trading Bot

A practical architecture for building a paper trading bot around frozen strategy profiles, quote-aware options data, launch contracts, and daily review.

Paper Trading Bot Backtest Parity Runbook

A runbook for freezing a paper candidate, replaying benchmark sessions, classifying mismatches, and reviewing live paper drift.

Unusual Options Activity Scanner: What Actually Matters Beyond Volume

Most unusual options activity scanners over-rank raw volume. Premium, volume versus open interest, spreads, DTE, and quote context matter more.

How to Backtest Options Without Stale Contract Leakage

A research-to-product guide to historical contract discovery, as_of workflows, quote windows, and avoiding modern-chain leakage in options backtests.

Why Option Quotes Matter More Than Last Price

Last sale can be stale in options. Historical bid/ask quotes give execution-aware research the market context it actually needs.

Quote-Aware Options Fills: What Our Research Changed

How bid/ask-aware fill logic changed the CuteMarkets research process and why several broad strategy claims became narrower.

0DTE Options Backtesting Data Requirements

0DTE options backtests need historical contracts, strict timestamps, quote coverage, rejection reasons, and realistic fill assumptions.

OPEX Week Options Data: What to Measure Before Trading

Use OPEX dates as planning anchors, then measure listed expirations, open interest, spreads, trade activity, Greeks, and IV before trading.

cuteoptionstrats: A Public Research Note on a Curated Intraday Options Model

A close reading of the public cuteoptionstrats repository: the c36_quality model, option microstructure filters, evaluation metrics, and what the negative results actually teach.

The One Piece of Sharpe: What Months of Intraday Options Backtesting Actually Taught Us

What did months of intraday options backtesting actually teach us? A few narrow sleeves survived, and many more ideas did not after months of audits.

Algorithmic Trading Research Log: How to Build in Public Without Hiding Failed Results

A strong algorithmic trading research log publishes failed ideas, exact gates, and changing conclusions instead of hiding dead ends from readers.

Building a Portfolio of Trading Models: Why One Good Backtest Is Not Enough

One good backtest is not enough. A portfolio of trading models needs low overlap, believable diversification, and hard promotion gates over time.

Gap Up Failure Fade Backtest: The Difference Between Intuition and Evidence

This gap up failure fade backtest shows how an intuitive reversal setup failed once VWAP, timing, and robustness rules were enforced in the repo.

Gap Reclaim Strategy Backtest: Why a Good Chart Pattern Failed the Data

A gap reclaim strategy can look convincing on charts and still fail the data. This post explains the c26 logic and why it did not survive in the repo.

Failed Trading Strategies: 7 Ideas We Tested So You Do Not Have To

Seven failed trading strategies from the repo, including zero-trade lanes and no-feasible-profile ideas, with the exact reasons they died in testing.

Why c4 Was Parked: A Dispersion Strategy That Improved But Still Failed the Portfolio Gate

c4 improved after repairs, but the dispersion strategy still failed the portfolio gate. Here are the exact conditions that blocked promotion in practice.

Relative Strength Breakout Strategy: Testing Proxy-Based Intraday Breakouts With QQQ and DIA

See how a proxy-based relative strength breakout strategy was tested with beta-adjusted rules, QQQ strength, and DIA benchmarking in repo runs directly.

Dispersion Trading Backtest: QQQ vs SPY and Why the Signal Was Not Symmetric

This dispersion trading backtest found a real QQQ edge and a weak SPY sleeve. The signal was not symmetric across indexes or overlays inside the repo.

VWAP Z-Score Strategy: How We Evaluated c36 and Why It Still Was Not Promoted

The c36 VWAP z-score strategy made money, yet it still was not promoted. Trade density and portfolio standards were the blockers in the portfolio ladder.

Intraday Mean Reversion Options: Why Signal Quality Drops When You Chase Density

Intraday mean reversion options can look strong until you widen the sample. This post shows how density often erodes the original edge in options research.

VWAP Mean Reversion Backtest: The Logic, the Edge, and the Failure Modes

This VWAP mean reversion backtest shows a real edge with a real weakness: the best-quality branch stayed too sparse to earn promotion in the repo.

Why Most Opening Range Breakout Strategies Fail Under Realistic Options Fills

Most ORB options strategies fail once fills become causal. See how DTE choice, stop logic, and execution filters changed the repo's results in practice.

Does Opening Range Breakout Still Work? Evidence From 0DTE and 5-Minute Tests

Does ORB still work after realistic execution fixes? Only in a narrow slice. This post compares broad 0DTE failures with tighter 5-minute lanes and setups.

Opening Range Breakout Backtest Results: What Survived After Realism Fixes

Opening range breakout backtest results changed sharply after realism fixes. Here is the narrow ORB pocket that still survived in the repo under pressure.

Strategy Robustness Testing: PBO, Deflated Sharpe, and Overlap Filters Explained

PBO, Deflated Sharpe, and overlap filters matter because profitable models still fail promotion. This post explains the repo's actual gates in production.

How to Avoid Overfitting in Trading Backtests With Walk-Forward Validation

Walk-forward validation, PBO, and DSR expose overfitting before a good-looking strategy reaches paper. This post shows what those failures look like.

Walk-Forward Backtesting: How to Test a Trading Strategy Without Fooling Yourself

Walk-forward backtesting tests a strategy without flattering it. Use OOS windows, rolling validation, and hard gates instead of one long sample alone.

Backtest vs Paper Trading: Why Good Trading Results Break in Live Markets

Backtest vs paper trading is mostly a realism problem. See how parity checks, execution drift, and promotion gates expose weak models early in practice.

Historical Options Backtesting: Data, Fills, and Slippage That Actually Matter

Historical options backtesting needs contracts, quotes, trades, and timing rules. This guide explains the data stack behind causal options research.

What Is Realistic Options Backtesting? A Practical Guide for Serious Traders

Learn what realistic options backtesting requires, from causal fills and strike selection to slippage controls and leak prevention in repo audits.

Earnings Options Plays, Scientifically: Measuring Implied Move, IV Crush, and Execution Quality with CuteMarkets

A research-style framework for earnings options trades using CuteMarkets, from implied-move estimation and structure selection to liquidity diagnostics and post-event evaluation.

Understanding Options Greeks: A Developer's Guide to Live Data

Delta, gamma, theta, and vega are the four pillars of options pricing. Learn how to consume real-time Greeks from the CuteMarkets API and build risk dashboards that respond to market movement.

Why Real-Time Options Data Is the Edge Retail Traders Are Missing

Stale quotes can cost you hundreds of dollars per trade. We break down the hidden latency in free data sources and show exactly what "real-time" means for options pricing.

Build a Put/Call Ratio Scanner in Under 50 Lines of Python

Put/call ratio is one of the oldest sentiment indicators in options markets. Here's how to build a live scanner that flags unusual sentiment shifts across an entire watchlist.

Our Algotrading Journey

Episode 10: The Current Crew

The current map of survivors, near-misses, and research-only sleeves as the portfolio journey becomes concrete.

Episode 9: Why QQQ Beat SPY In Dispersion Options

Once quote loading, overlays, and parity drift were repaired, QQQ kept the signal while SPY did not.

Episode 8: c36 And c4, Promising Is Not Deployable

c36 and c4 showed two different kinds of near-miss, proving that promising and deployable are not the same thing.

Episode 7: Failure Week Was Productive

A week of explicit closures that saved time by turning weak or sparse branches into reusable negative results.

Episode 6: c66, The First Real Anchor

Why c66 became the first real portfolio anchor: stable stress behavior, enough trades, and operational progress past research-only status.

Episode 5: From Frontier Search To Portfolio Thinking

The point where the project stopped optimizing one family harder and started assembling a believable, low-overlap portfolio.

Episode 4: ORB After The Audit

After realism fixes, broad ORB mostly failed and only a narrow, constrained pocket remained defensible.

Episode 3: The Simulator Audit

A hard audit of the simulator fixed leakage, aggregation, and selection bugs that had been overstating confidence.

Episode 2: Speed Before Alpha

Research speed, dashboards, and observability improved first, making later falsification cheaper and more credible.

Episode 1: Building The Ship

How the repo stopped trusting low-fidelity options backtests and started treating execution realism as core research, not cleanup.

Ready to start building?

Get a free API key and make your first request in under a minute.

Get started free